Smart Tips About Consolidated Statement Of Comprehensive Income

Free 8+ Statements Samples In Pdf

Free 15+ Sample Statement Forms In Pdf Ms Word Excel

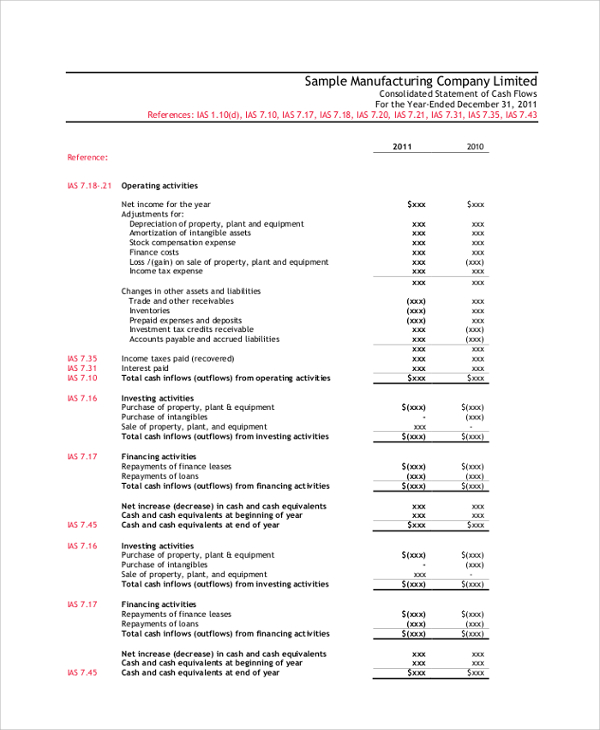

Consolidated Financial Filinvest Development Group

Statement Of Comprehensive Overview, Components And Uses

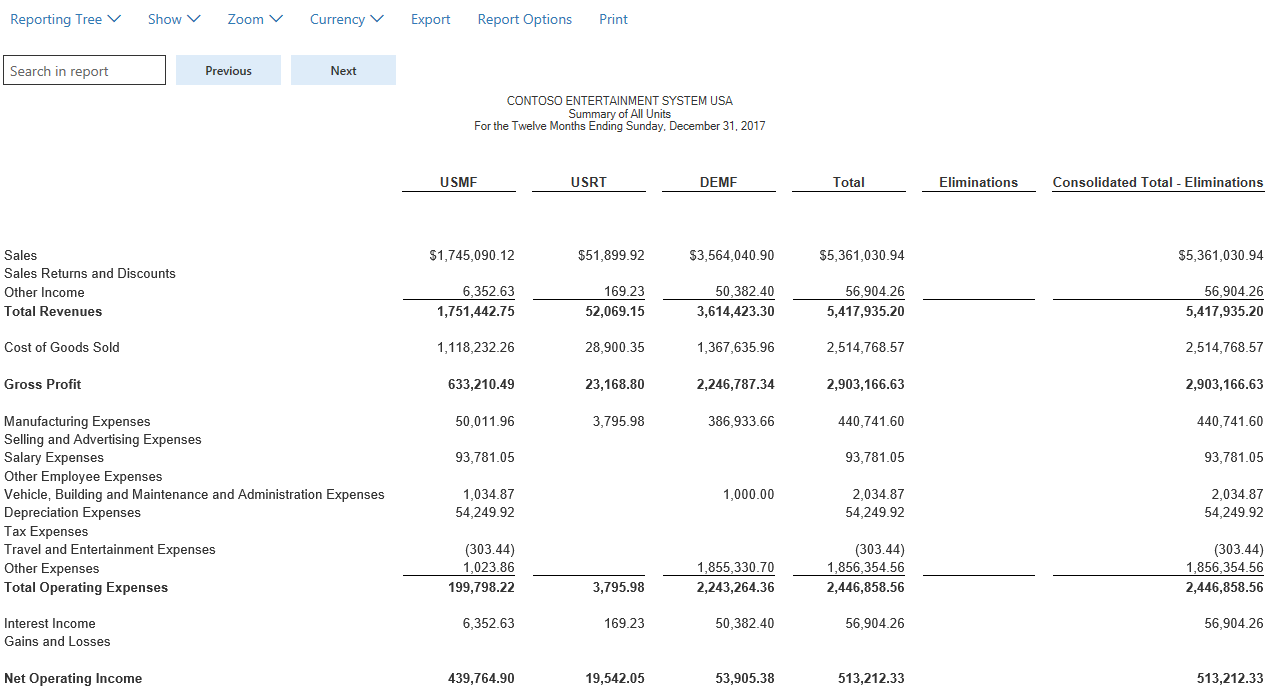

Generate Consolidated Financial Statements Finance Dynamics 365

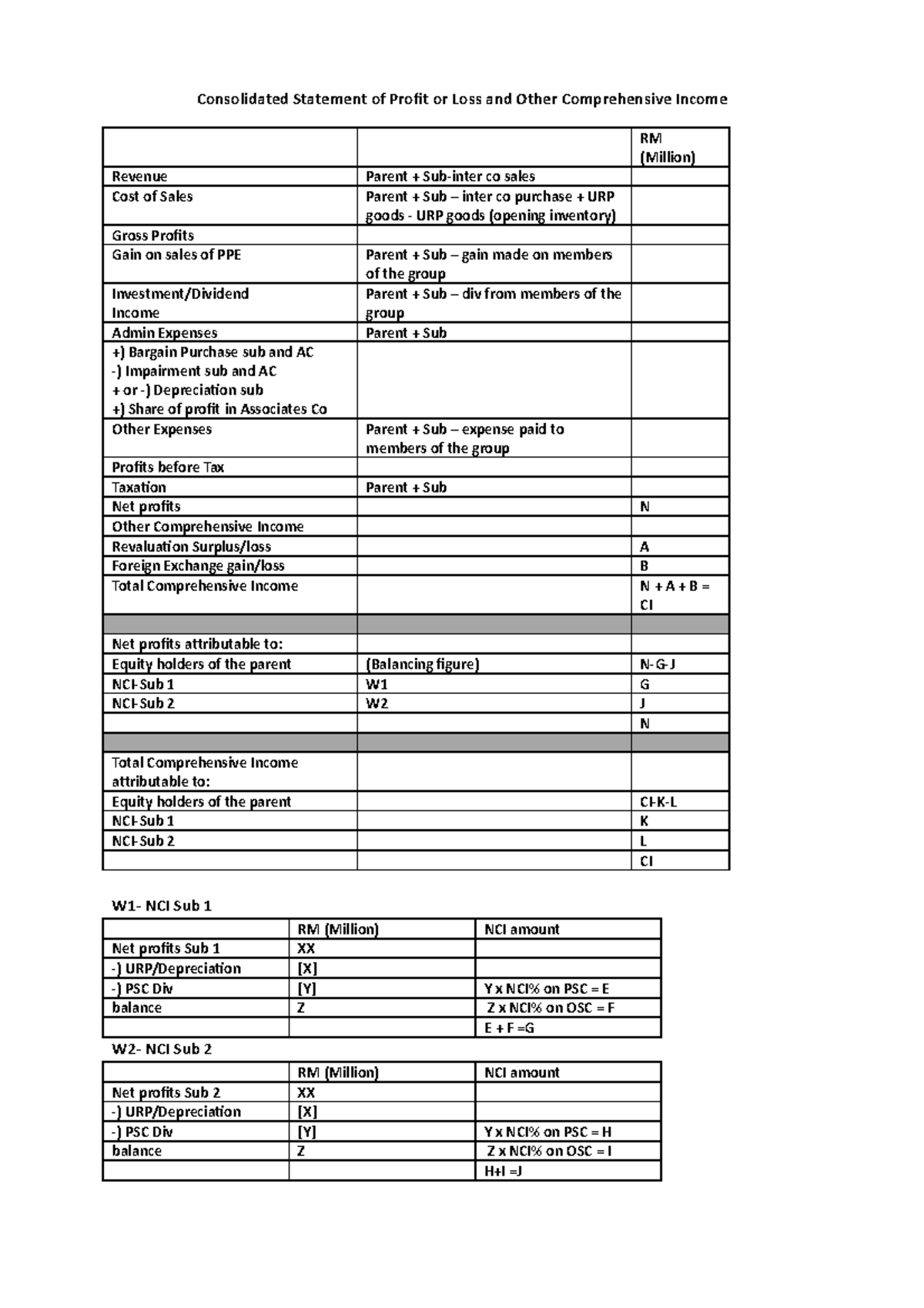

Consolidated Of Statement Profit Or Loss With Examples

Share of other comprehensive income of joint ventures and associates.

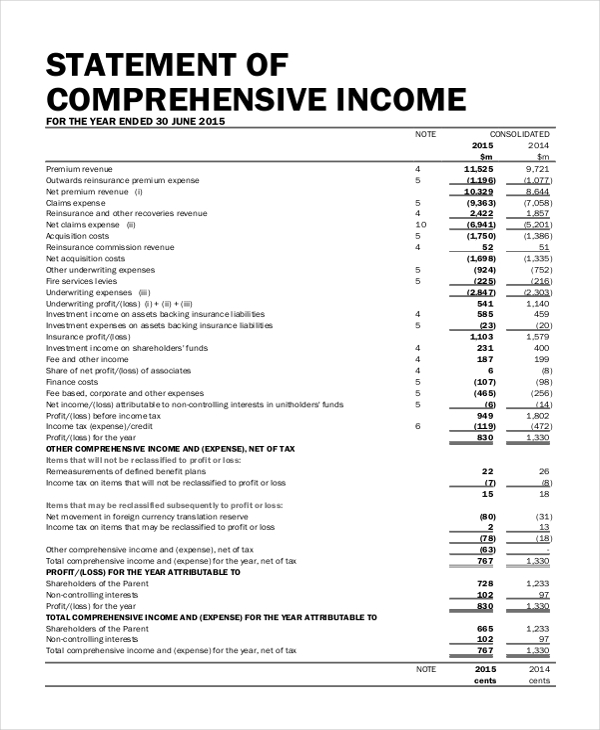

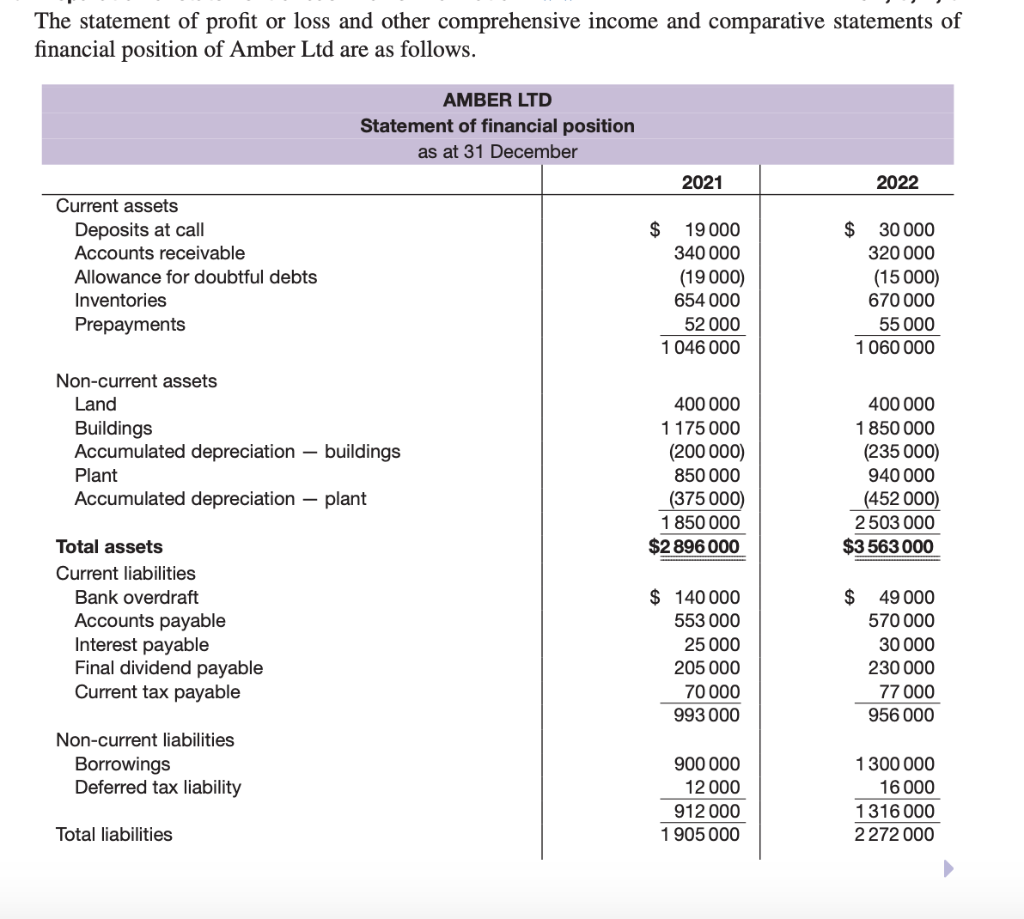

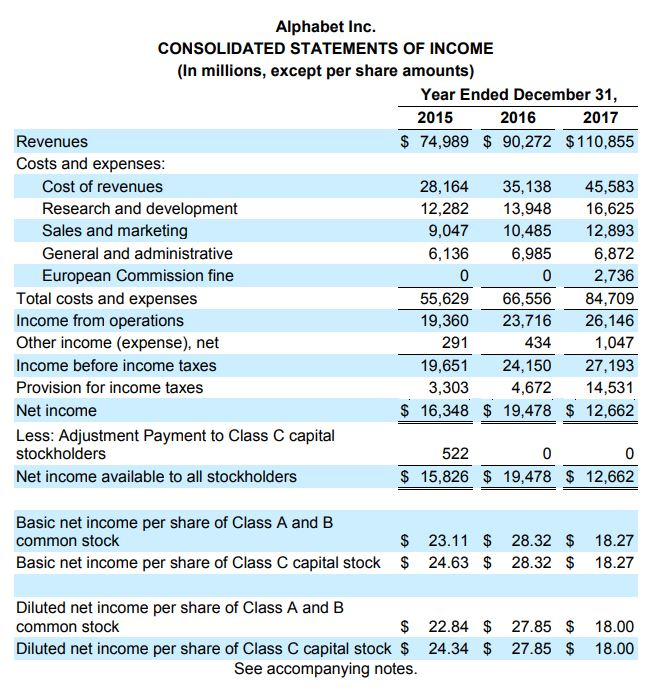

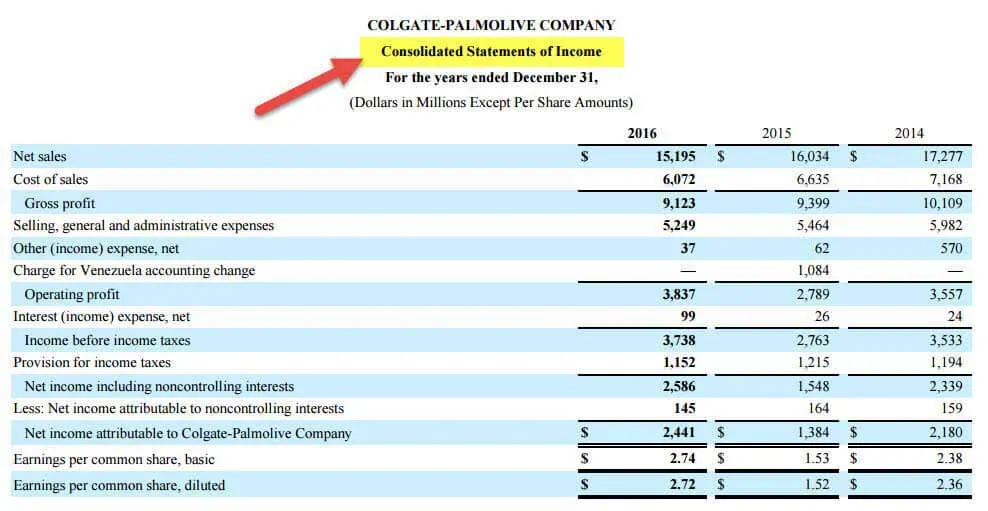

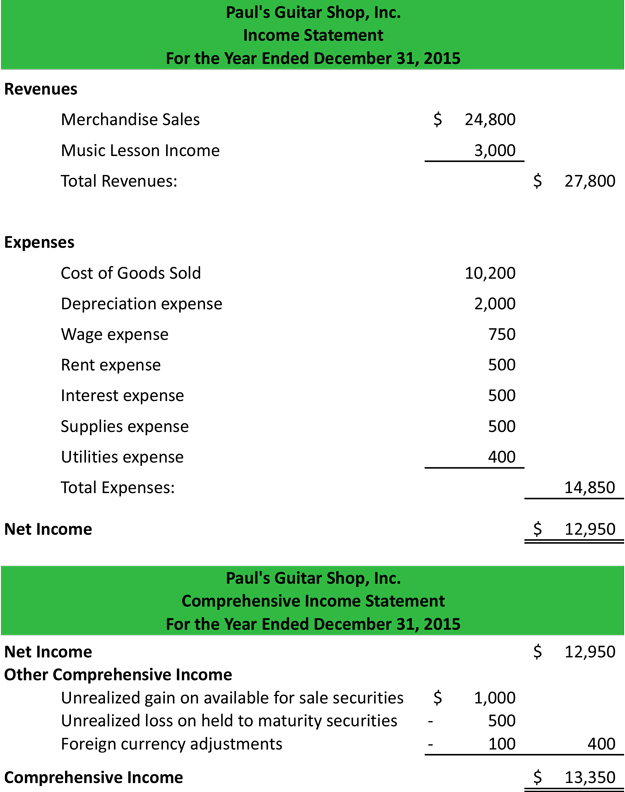

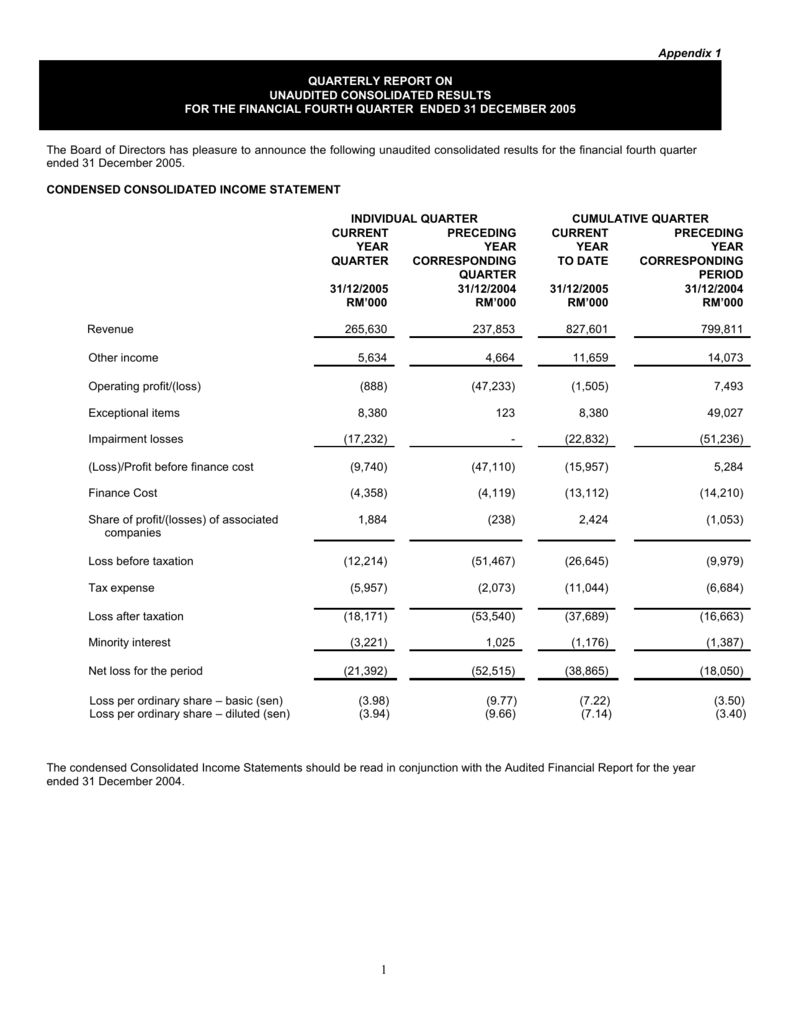

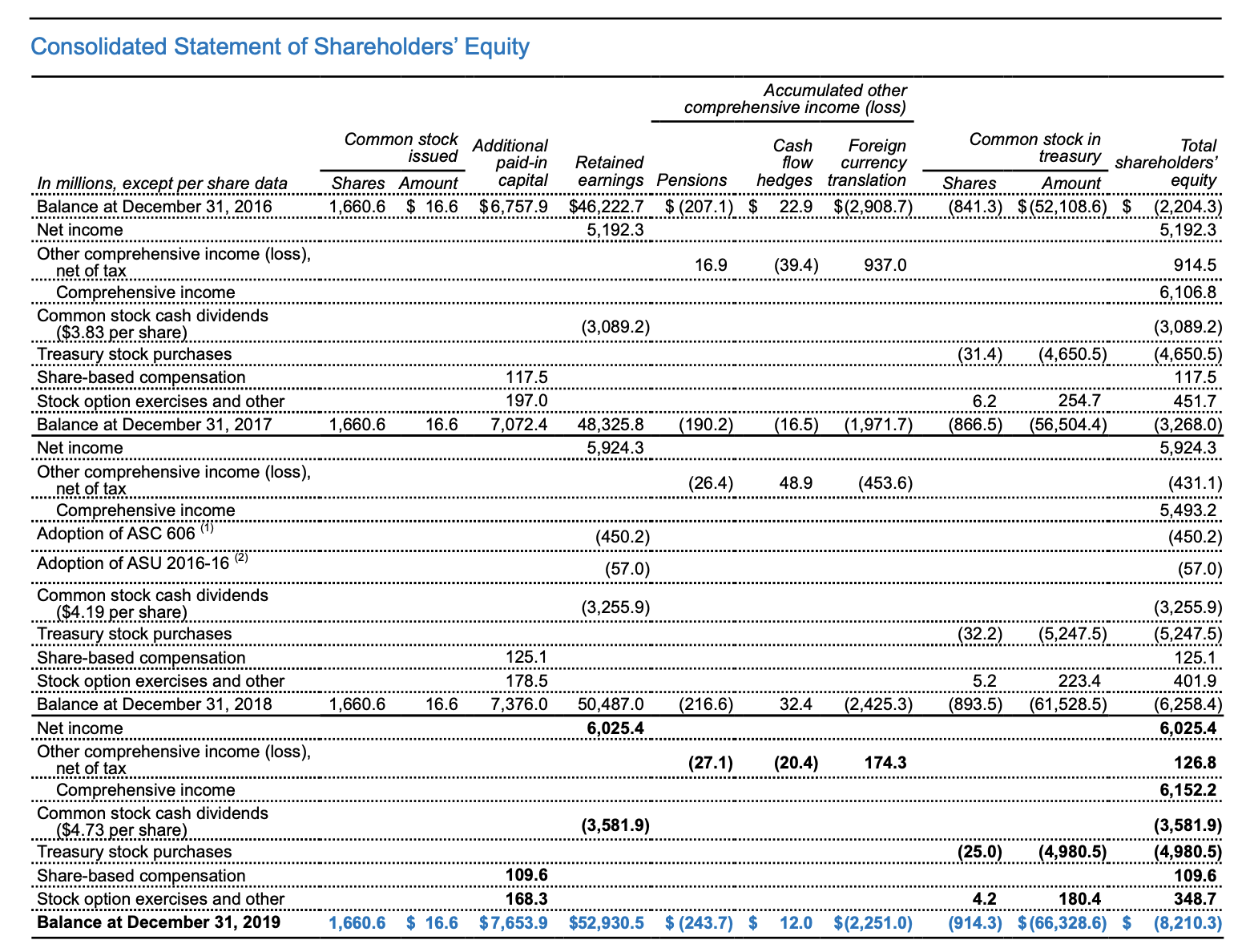

Consolidated statement of comprehensive income. The statement of retained earnings includes two key parts: Statement of comprehensive income refers to the statement which contains the details of the revenue, income, expenses, or loss of the company that is not realized when a company prepares the financial statements of the accounting period, and the same is presented after net income on the company’s income statement. The statement of comprehensive income reports the change in net equity of a business enterprise over a given period.

Consolidated financial statements present assets, liabilities, equity, income, expenses, and cash flows of a parent entity and its subsidiaries as if they were a single economic entity. Share of other comprehensive loss of joint ventures and associates. It includes net income and unrealized income.

Describe the components of and prepare a consolidated statement of comprehensive income or extracts thereof including: These statements are prepared in accordance with ifrs 10. Items of other comprehensive income that will not be reclassified subsequently to profit or loss.

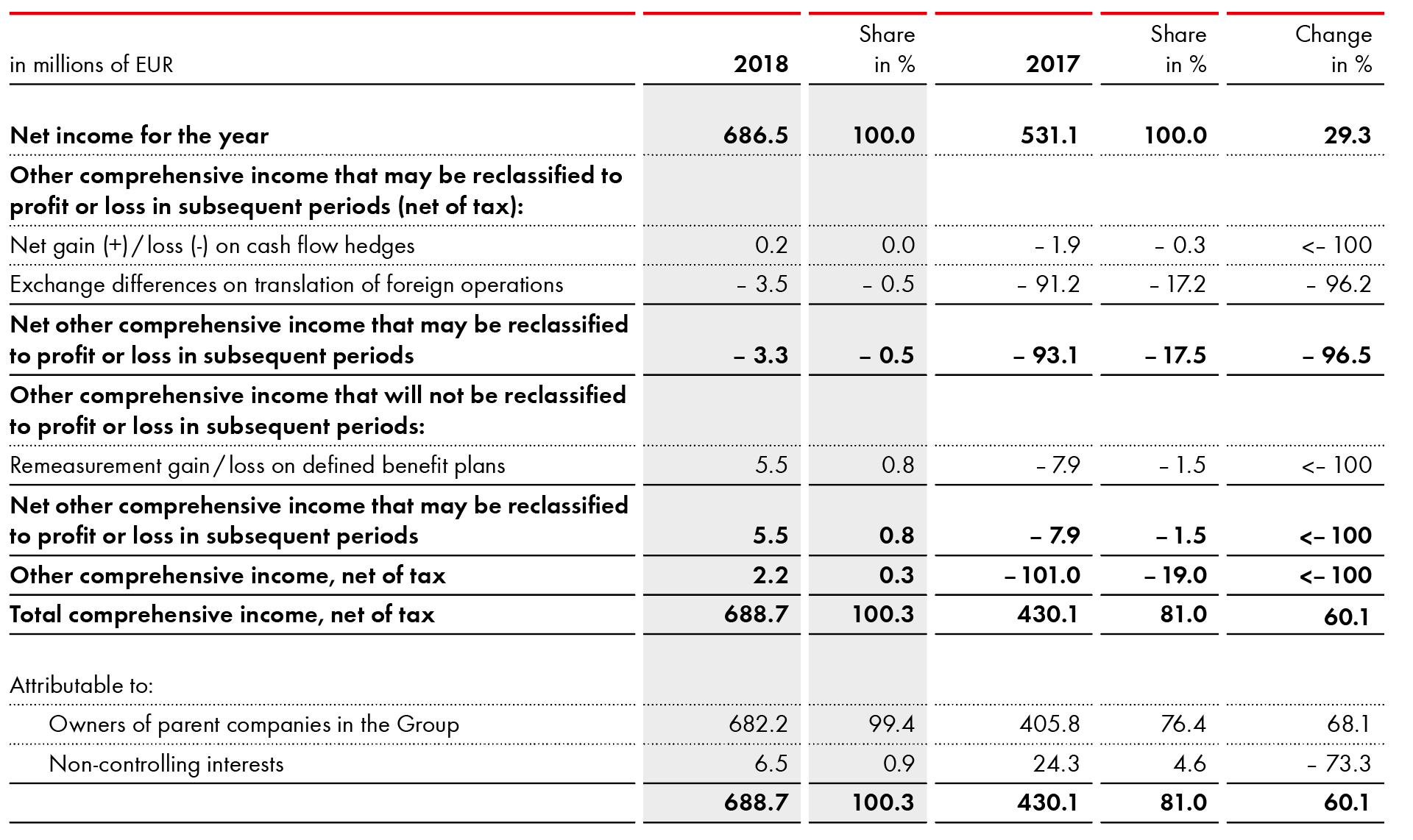

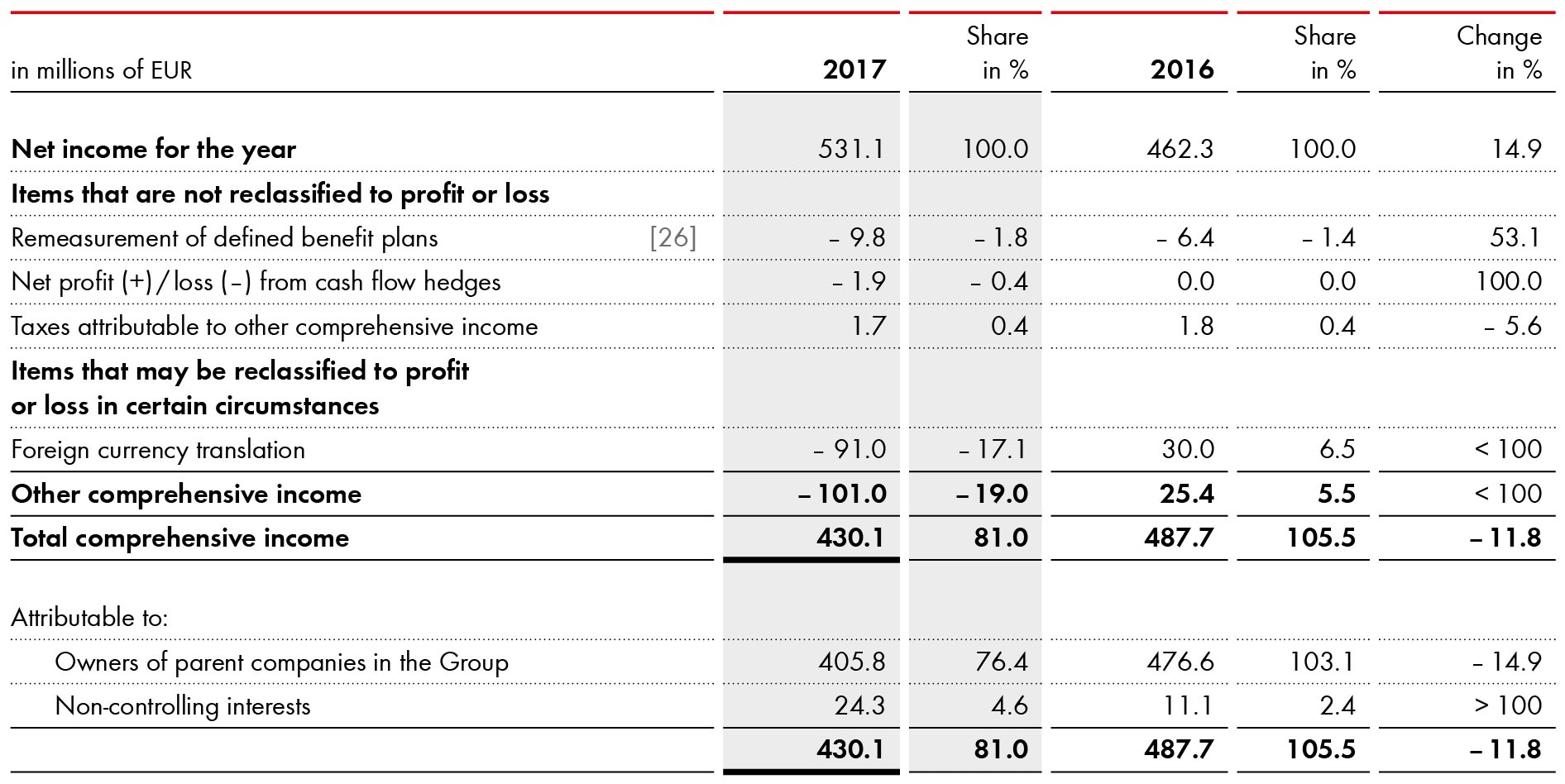

Adidas ag consolidated statement of comprehensive income (ifrs) € in millions. A separate statement of comprehensive income should begin with net income attributable to the consolidated reporting entity. If a reporting entity has nci, net income before nci would be the starting point for a separate statement of.

Consolidated statement of comprehensive income. Net income, and other comprehensive income, which incorporates the items excluded from the income statement. It introduces the subject and reproduces the official

Amazing Comprehensive Formula Dividends Received On Statement

Comprehensive Statement

Profit, Loss And Other Comprehensive Acca Global

Consolidated Statement Of Comprehensive

Consolidated Statement Us Gaap To Ifrs Source

Supreme Prepare Comparative Statement Of Profit And Loss Nike Cash Flow

Statement Of Comprehensive

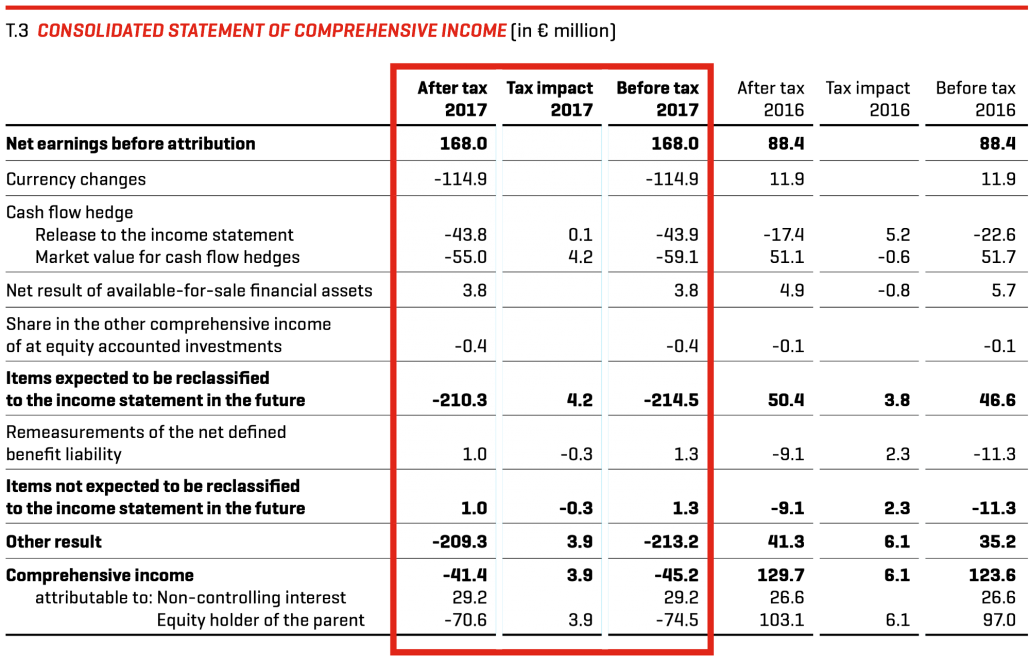

Consolidated Statement Of Comprehensive Puma Annual Report

Prepare The Consolidated Statement Of Profit Or Loss And Other

:max_bytes(150000):strip_icc()/CSI-5bb2f4e2eb5948bab0415f1b76e47bbf.JPG)

Financial Statements List Of Types And How To Read Them

Other Comprehensive Statement Example Explanation

Condensed Consolidated Statement

Solved Consolidated Statement Of Comprehensive In